Otto, 2023

Designing the end to end debt management experience

My role

Product Designer

Skills and tools

Figma, user research, prototyping

Problem space

B2C finance

Duration

6 months

Overview

About Otto

Otto is a financial mobile app that is focused around debt management, providing people with a birds eye view of their debts and providing recommendations on payments to make.

What I did

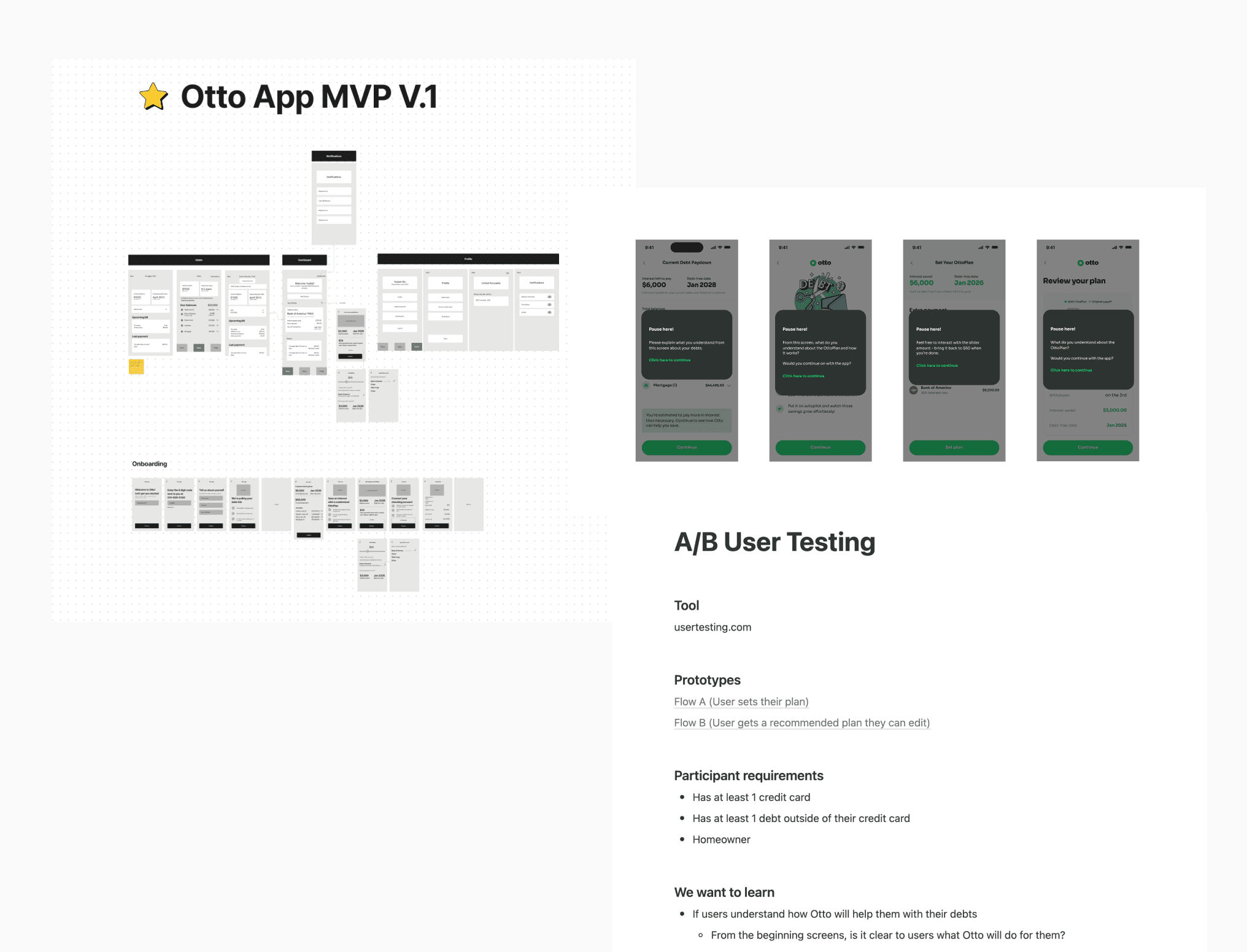

I was the sole product designer joining at the time of a pivot, so I rebuilt the app from ground up with a new design system and formed the design direction of the full app experience, from information architecture to user flows to high fidelity. I launched the MVP to paying user experience, iterated on the entire product from user feedback, and added new features based on improved backend functionality.

I worked directly with my CEO to form the product direction, a design mentor to advise on product management and visual feedback, and an engineer to implement & revise designs in QA.

Problem

Debt is a huge issue in America. Credit card debt is at an all time high, it’s a stressful and taboo subject, and tedious to manage.

Goal

Create a tool that helps people keep track of their debts and pay them off in a financially beneficial way.

Outcome

Designed an app where users can view all of their debts in one place with visibility to their interest rates, allocate a monthly amount for their payments according to their goals, and retained a 36.5% conversion rate for paying users.

User surveys and interviews

Understanding what makes debt difficult

We did an email survey with people who carried a balance from our previous user pool.

We wanted to understand:

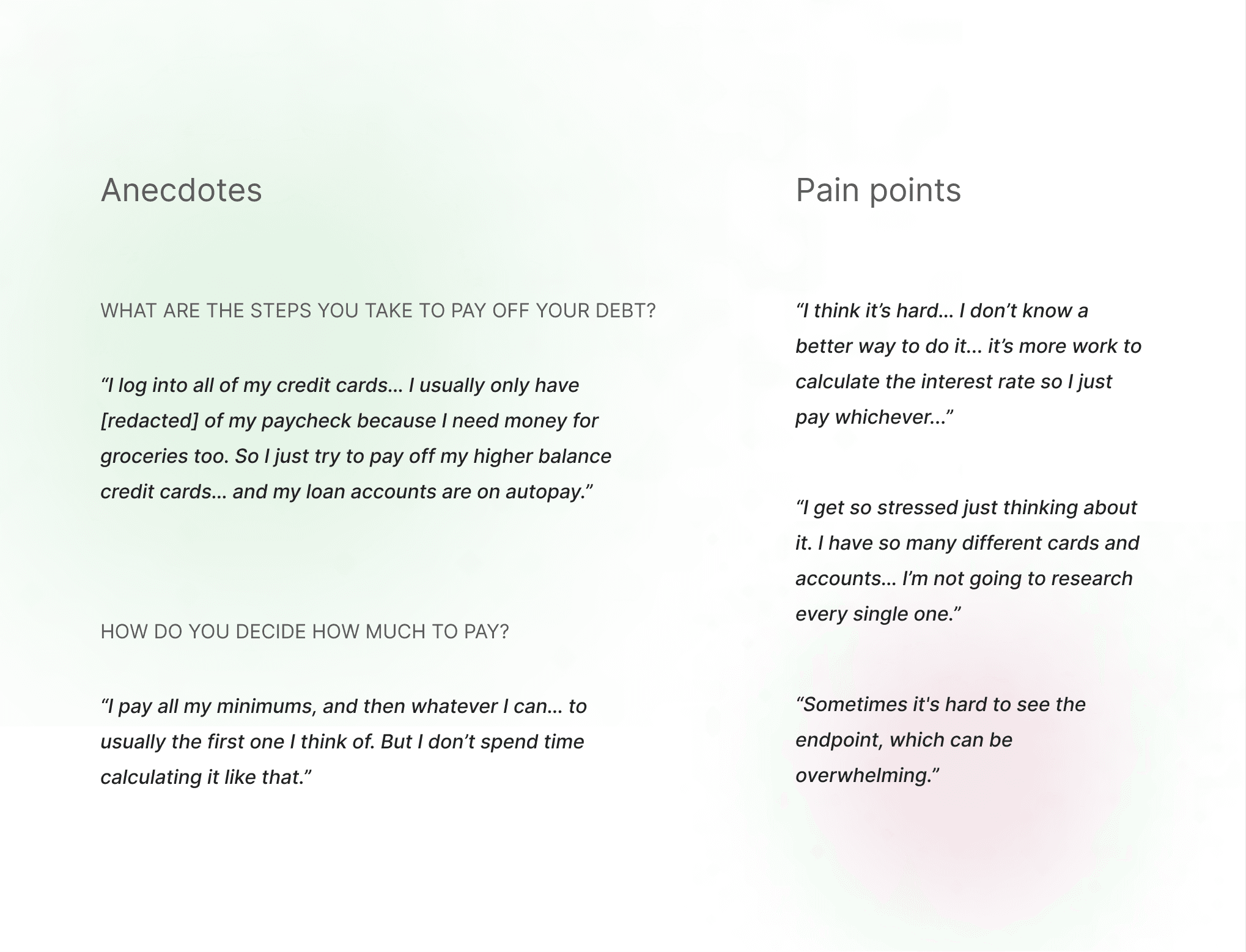

How are people currently paying their debts off?

What makes paying off debt stressful?

What are people’s main financial goals?

We also spoke to 2 people who completed the survey to get a more in depth understanding.

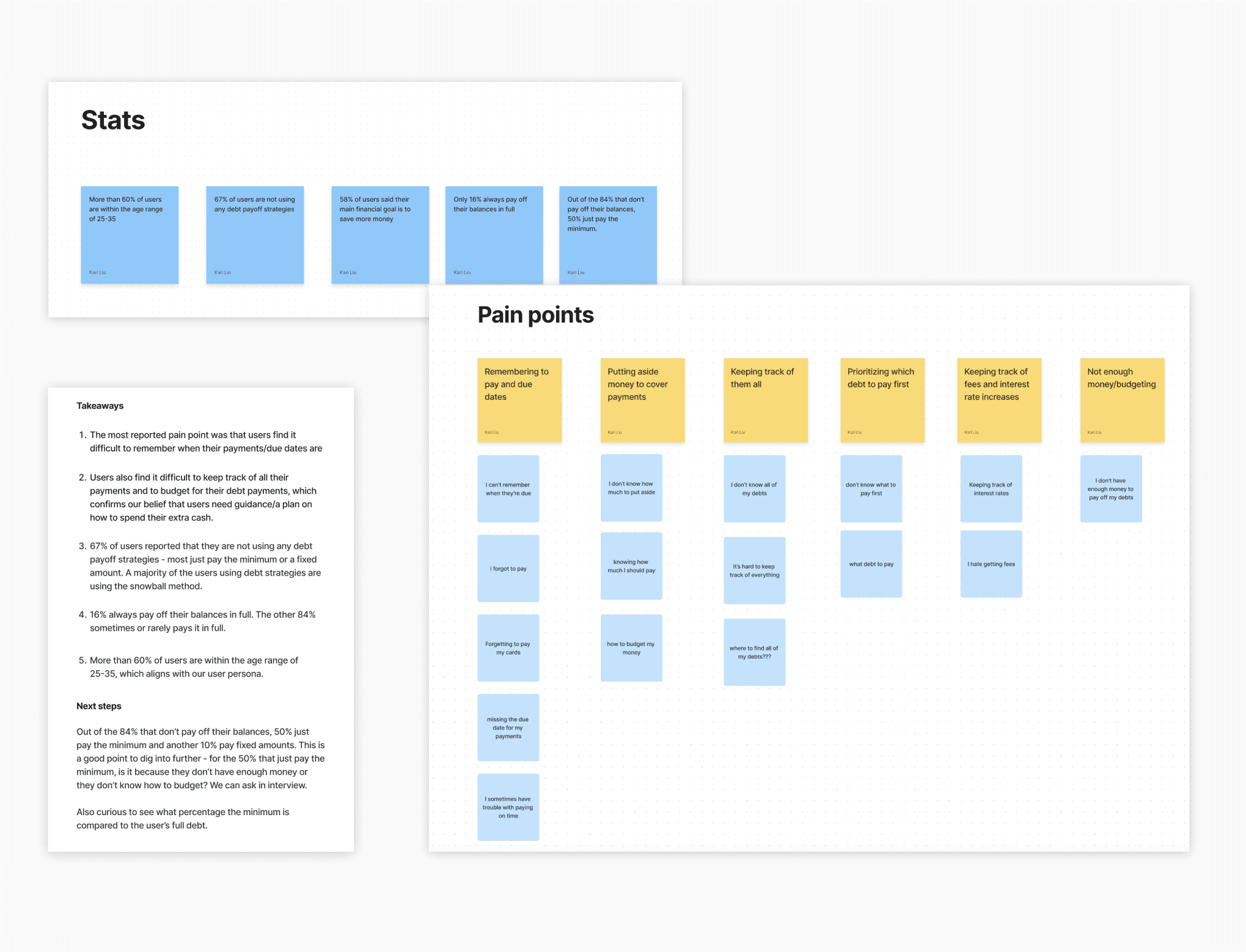

Takeaways

People care a lot about saving more money

Have trouble remembering when to pay their debts - the process is manual, since people have to log into each debt portal. only 20% of people set their debts to autopay - 67% of people were not paying down their debt by a strategy

We’re solving for people who can at least pay their minimums each month.

Key user stories

I find it difficult to keep track of what I pay because I have so many different debt lines. I want to see all of my debts in one place so I know where I am in my debt pay down progress.

I typically have money leftover after paying the required amount that I put towards my debt accounts, but I'm not sure if I'm doing it correctly. I want to know how to use my funds in a way that saves me more money.

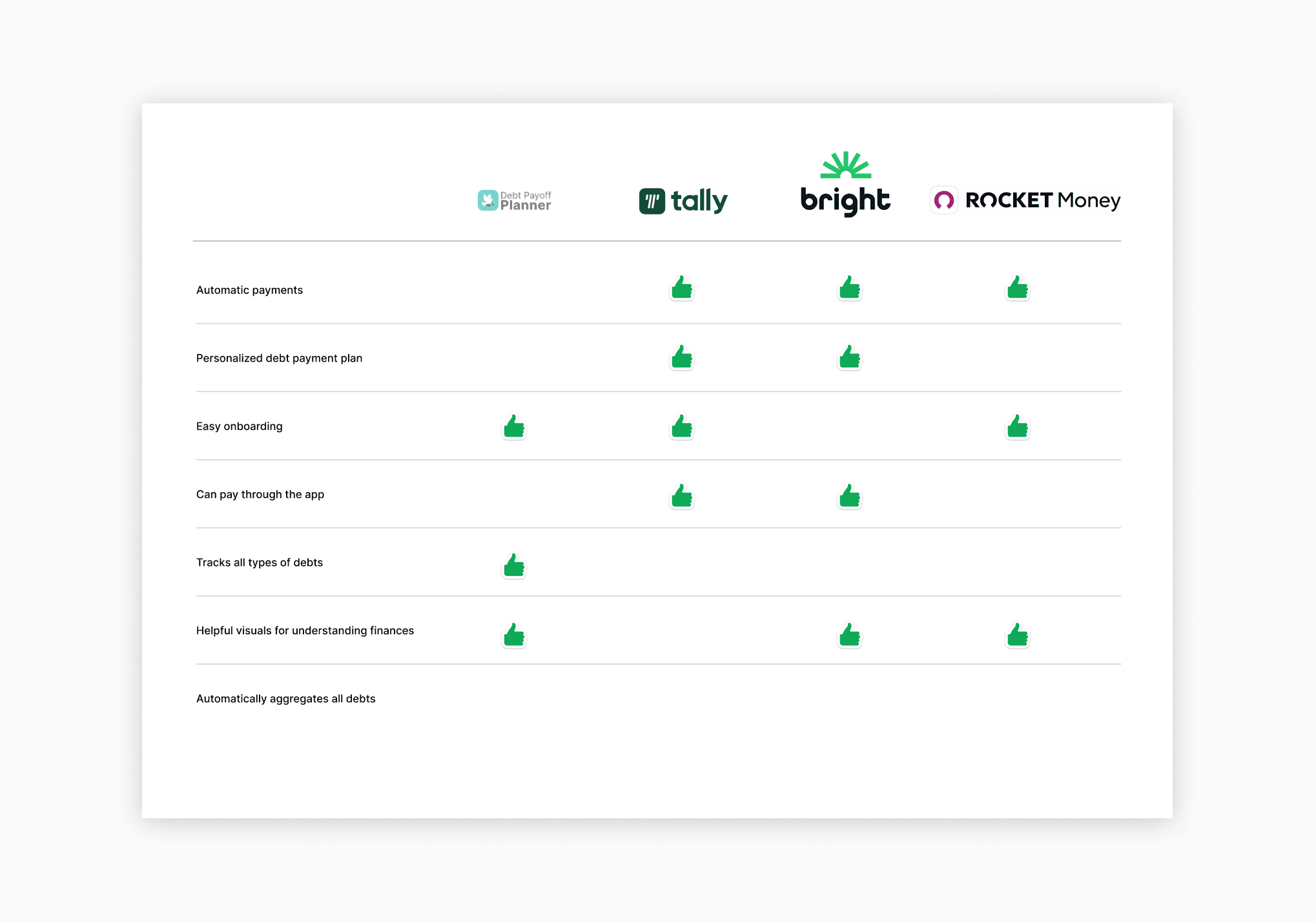

Competitive analysis

What debt management solutions are out there?

I examined potential competitors to learn about how existing products help people manage their finances and pay off debt. I used this audit to identify areas Otto can help users and to guide inspiration for onboarding patterns. I looked at Bright, Tally, RocketMoney, and DebtPayoffPlanner.

Takeaways

Apps like Bright and Tally focus on helping users get out of credit card debt, but no app currently helps people pay down all of their debts

There are apps like DebtPayoffPlanner that help users keep track of all of their debts, but this is a manual process and does not provide any insight on how to save money

Apps like RocketMoney are good at showing aggregate views and providing an overall view of finances, but doesn't target debt specifically

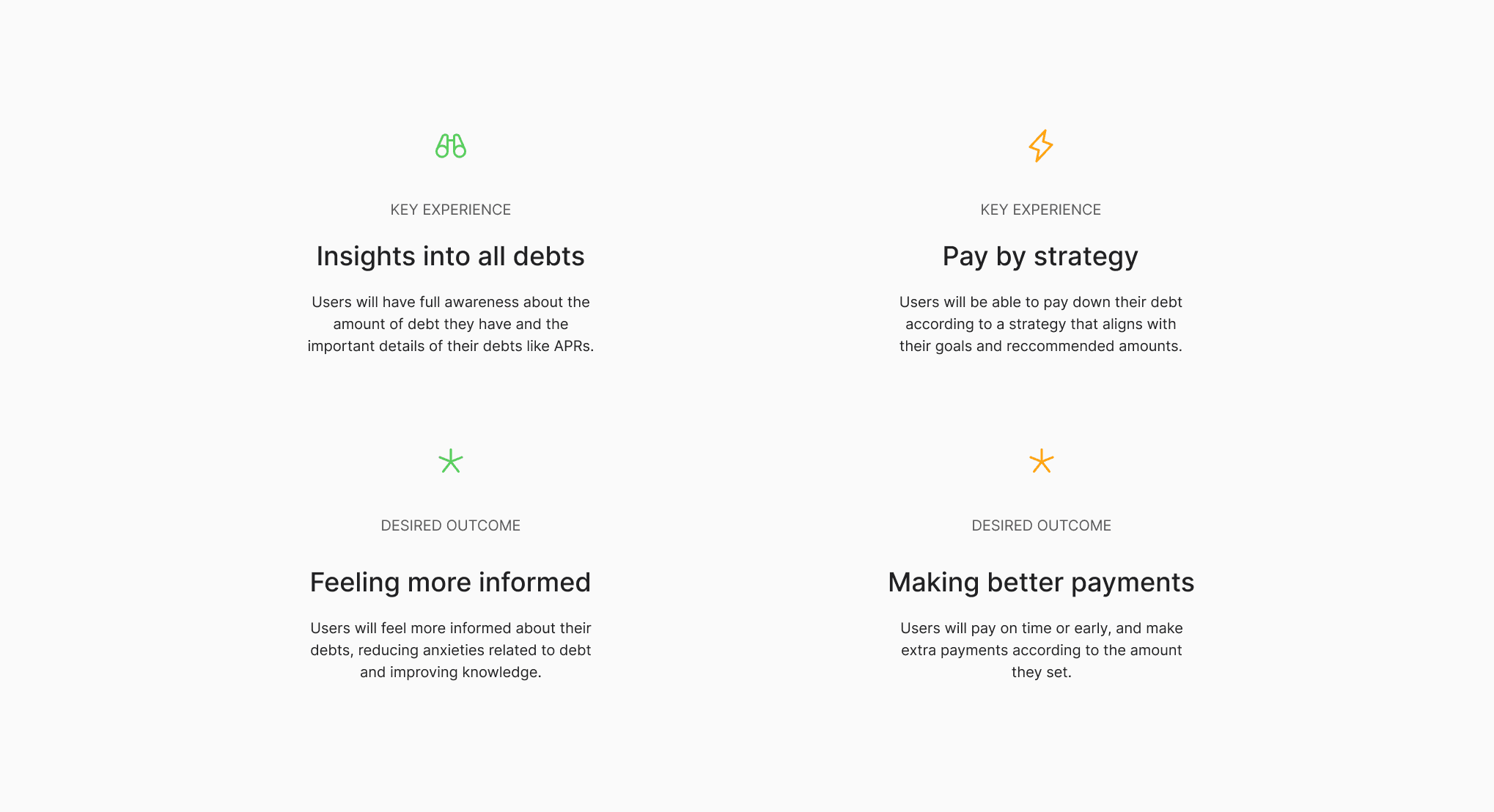

Goals and success metrics

What will a successful experience have?

Based on the research conducted, I distilled my insights into a few key experiences and success metrics:

Ideation and iteration

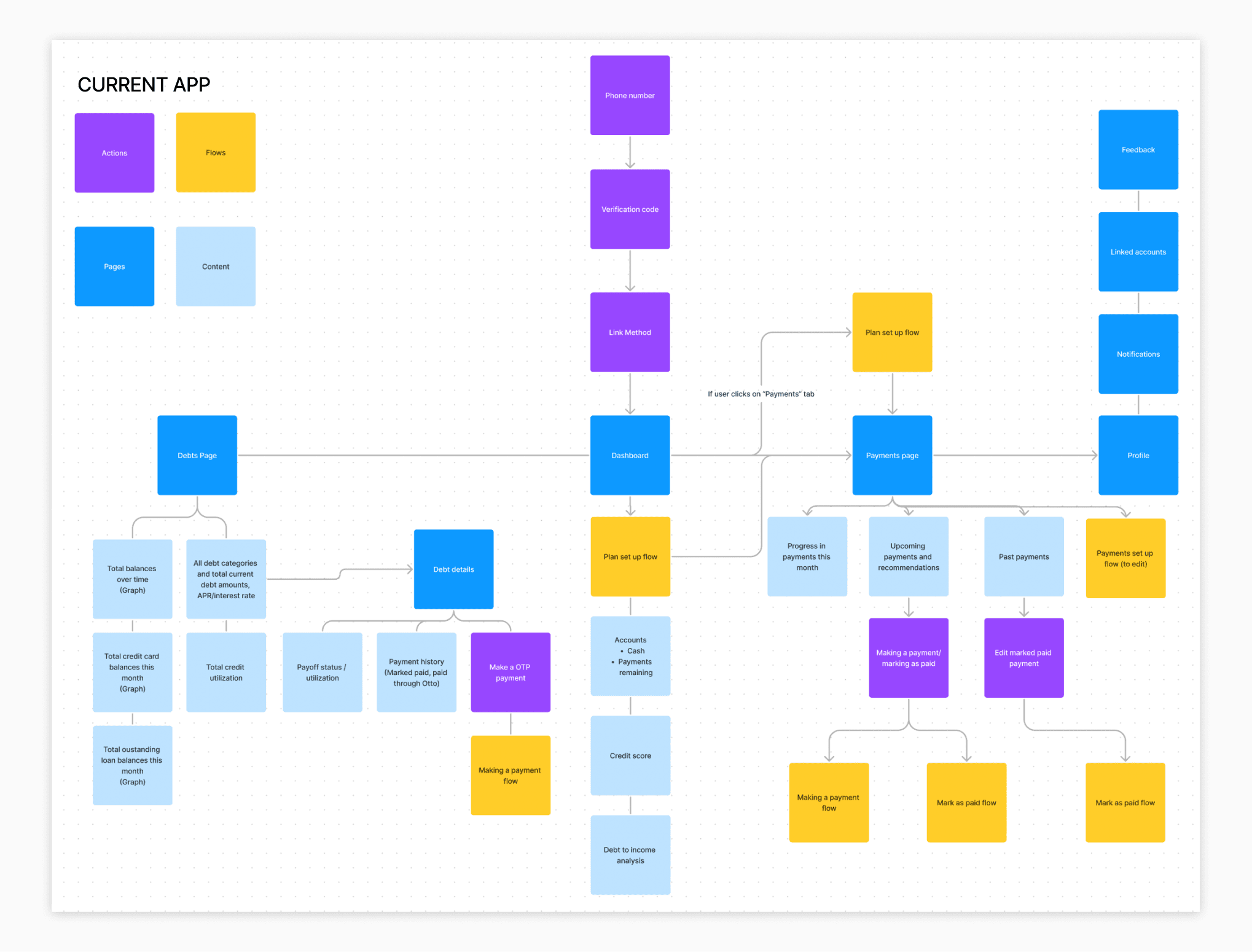

Designing the full experience

Improving onboarding

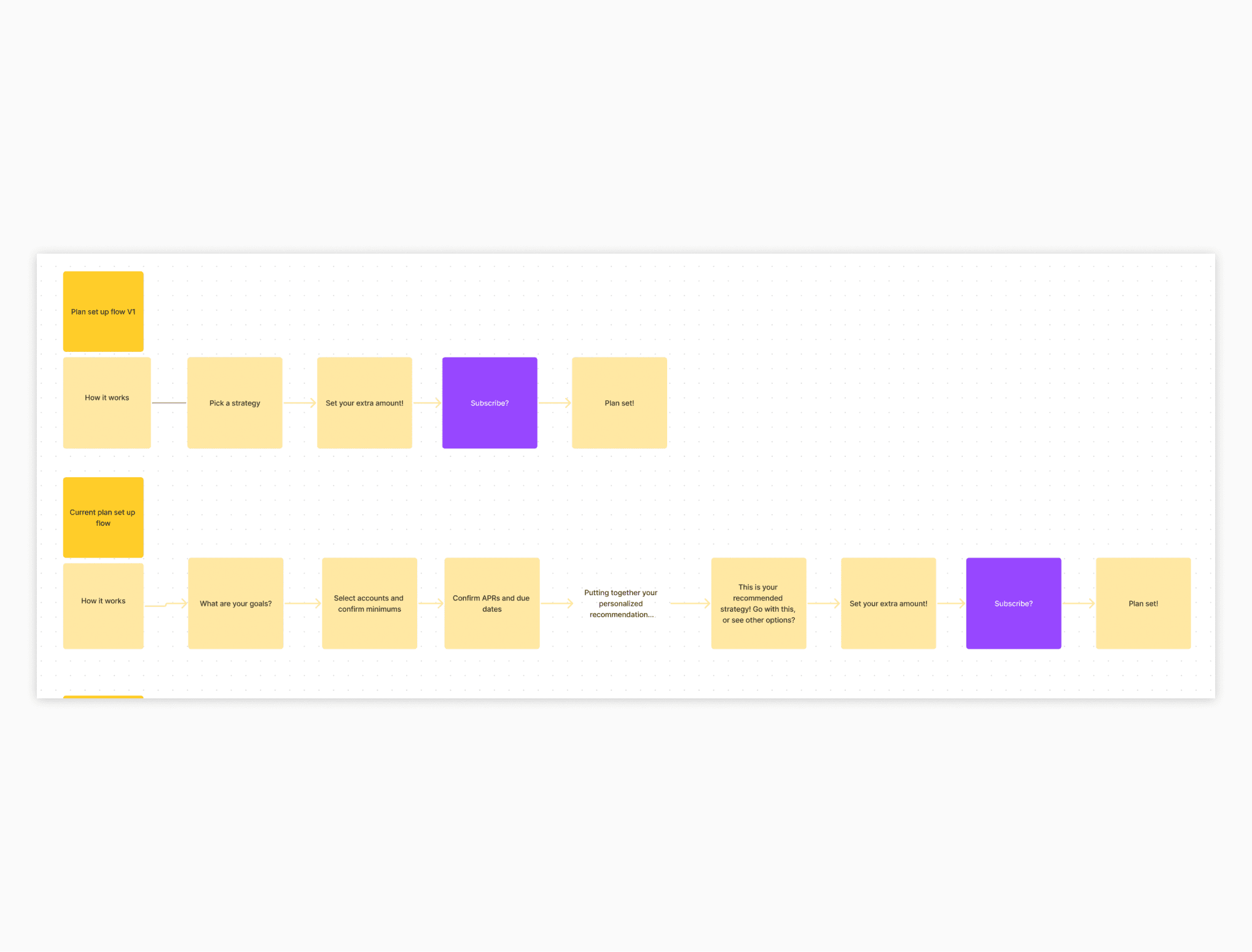

We had a longer onboarding in sign up to retrieve the necessary information to build their plan, but users were churning and dropping out halfway. We found that when we moved the payment plan onboarding out of sign up so that users could explore the app first, they were more willing to set up a plan.

Autonomy to decide or guided recommendations?

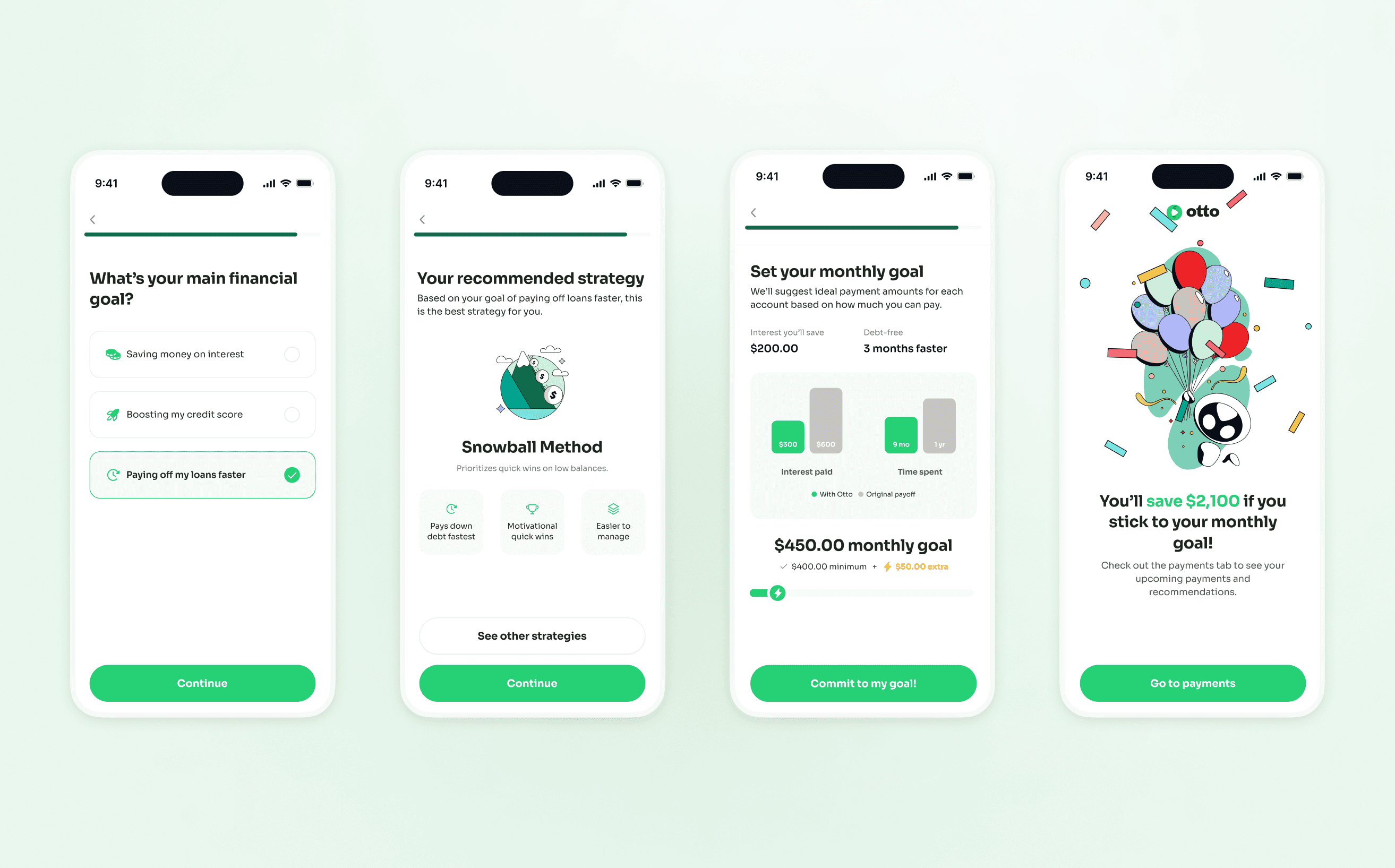

During this time, I conducted A/B testing to see if users preferred the autonomy to select their own plan, or receive a recommended plan tailored to their goals.

We found that receiving a recommended plan was more positively received.

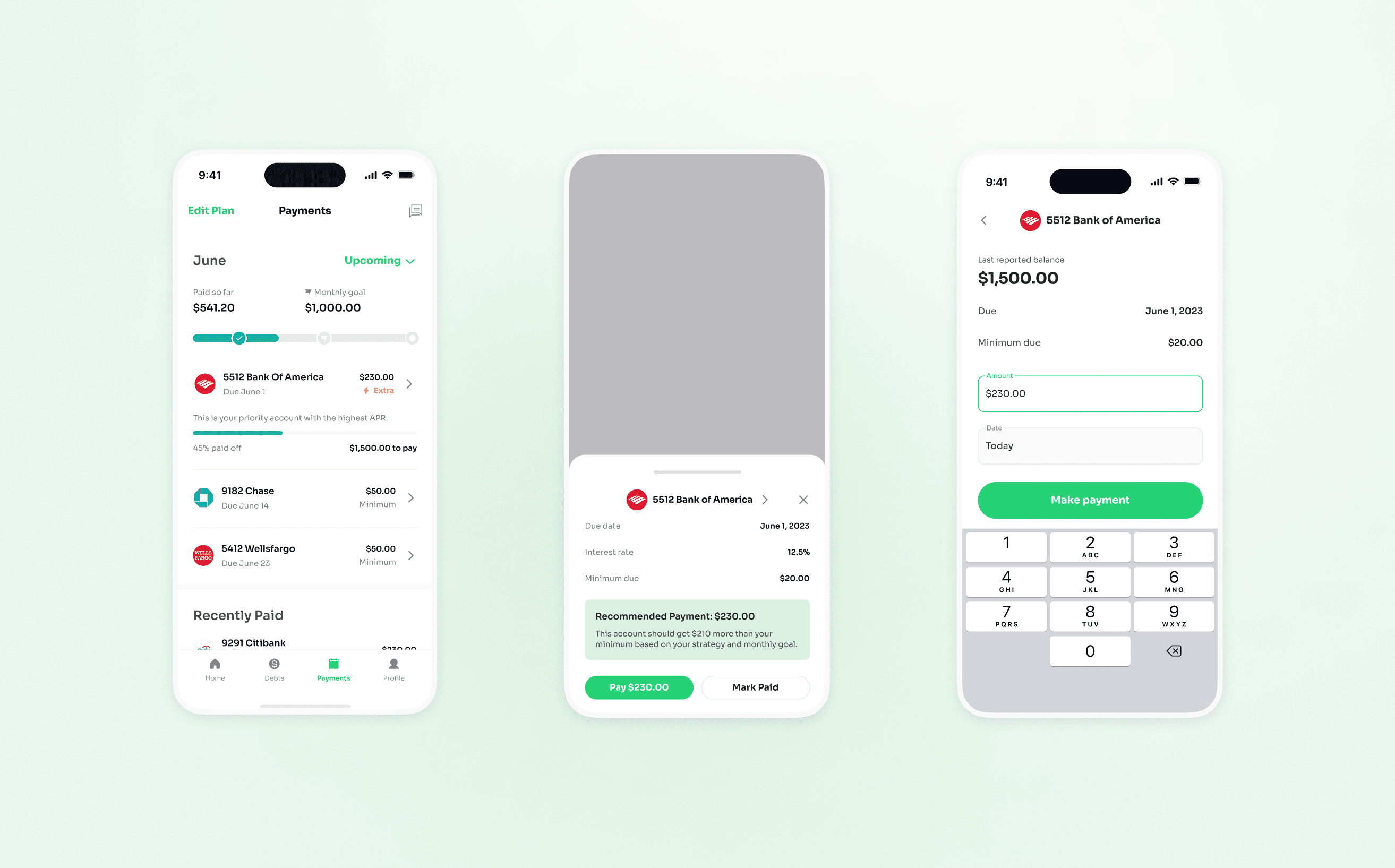

How users can pay off their debts

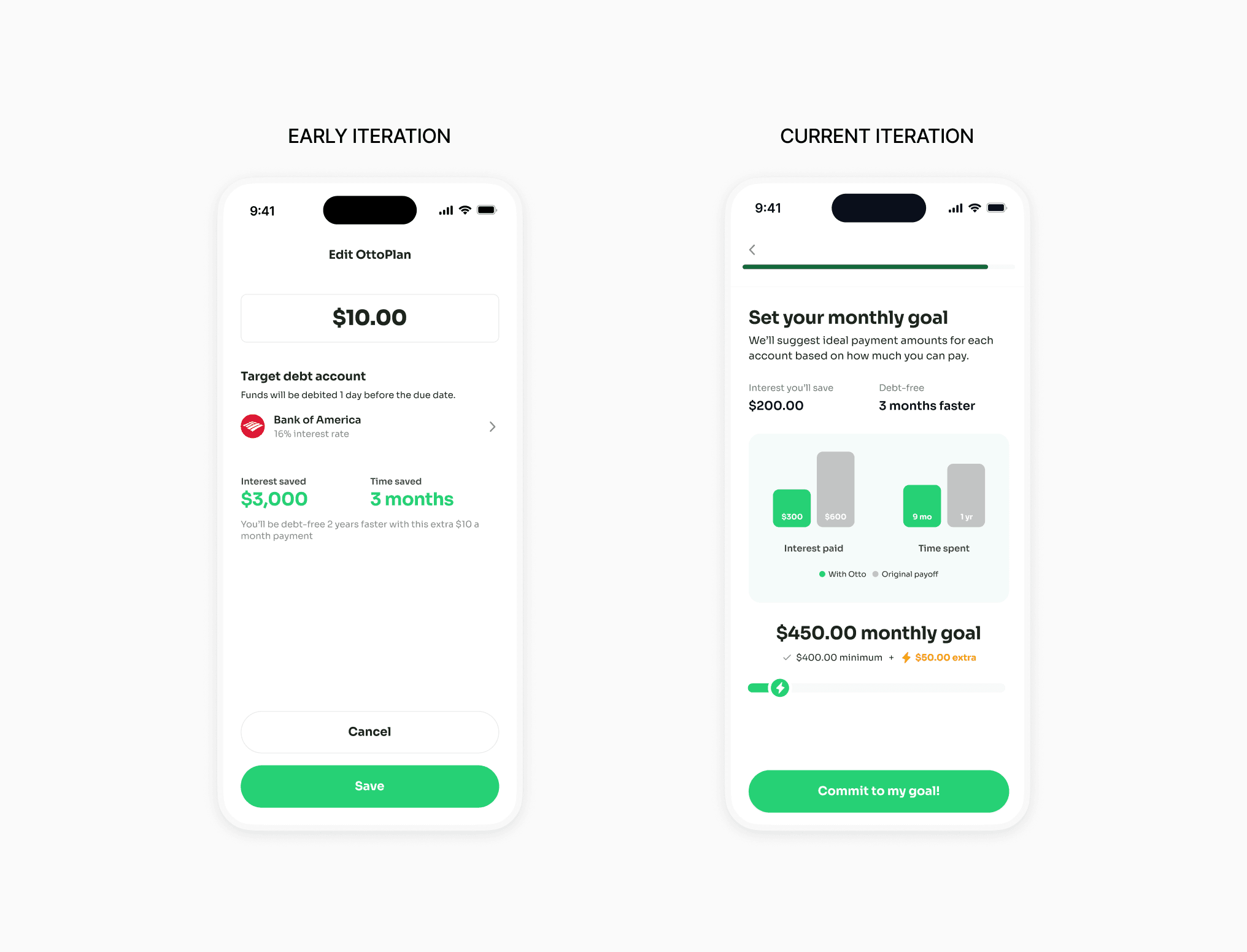

Initially, we only allowed users to pay a fixed extra amount to a single account. We found that users often didn’t want to set an extra amount, and that the fixed extra amount didn’t always just go to one payment. We wanted to provide a more holistic view of what the user had to pay by month.

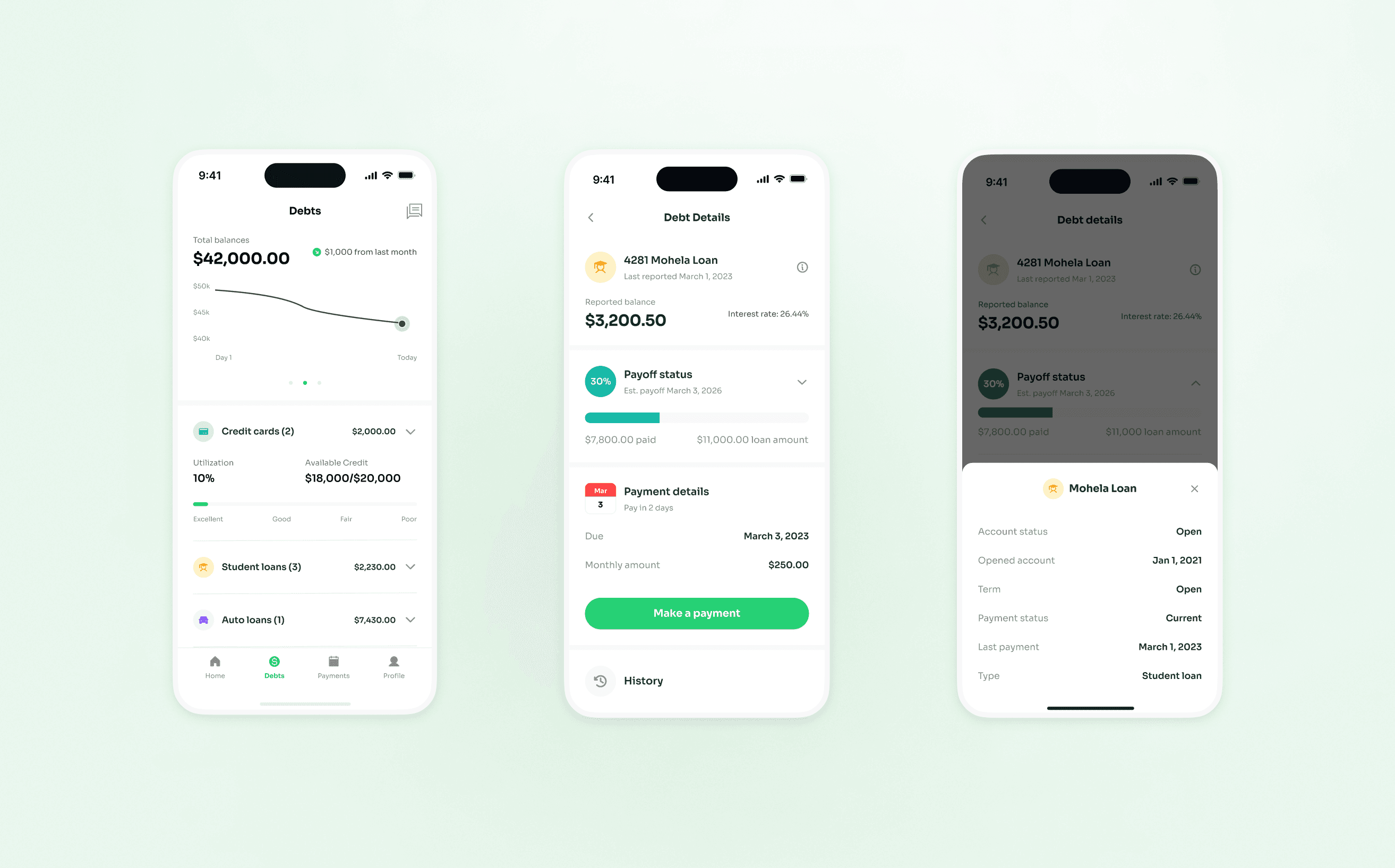

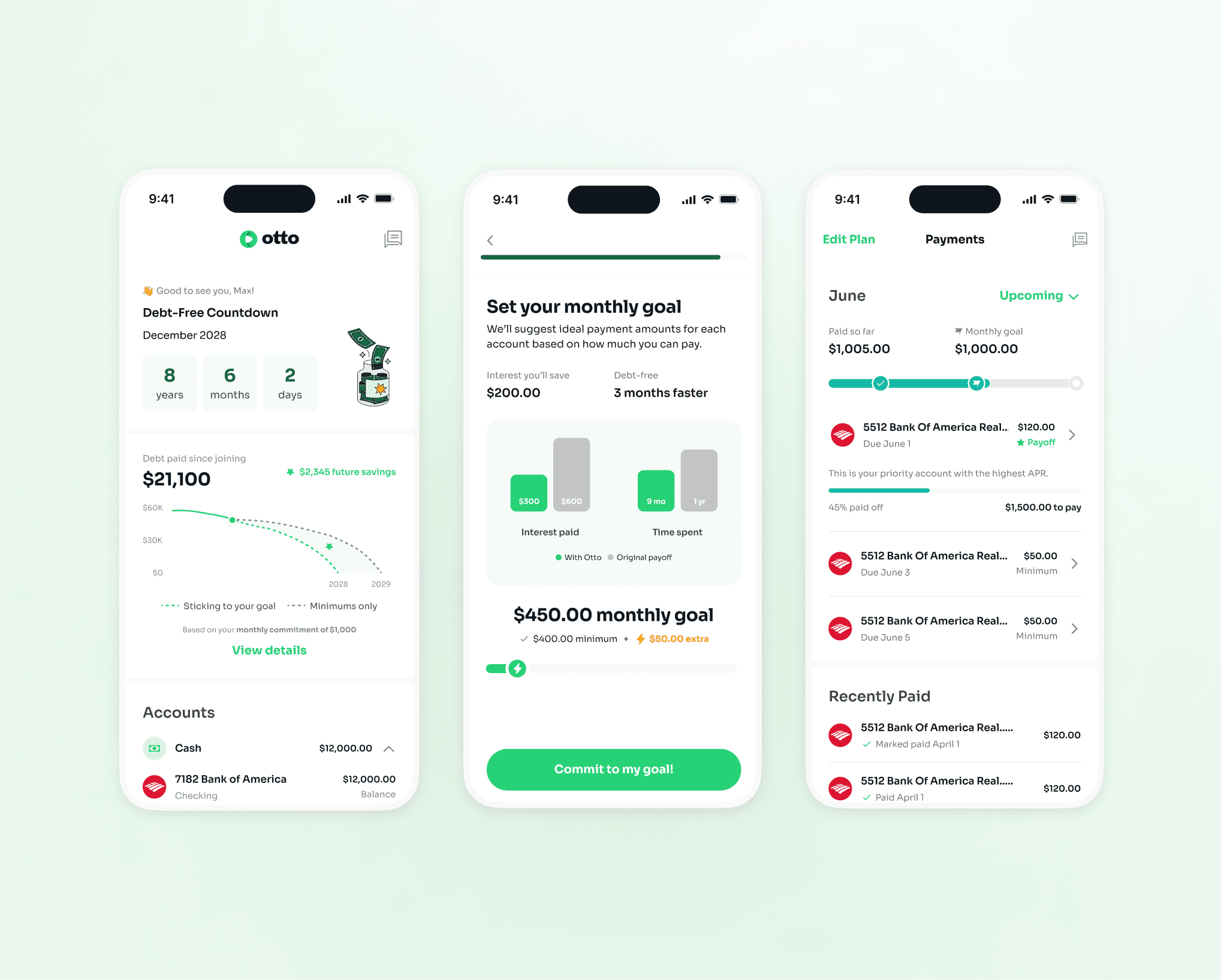

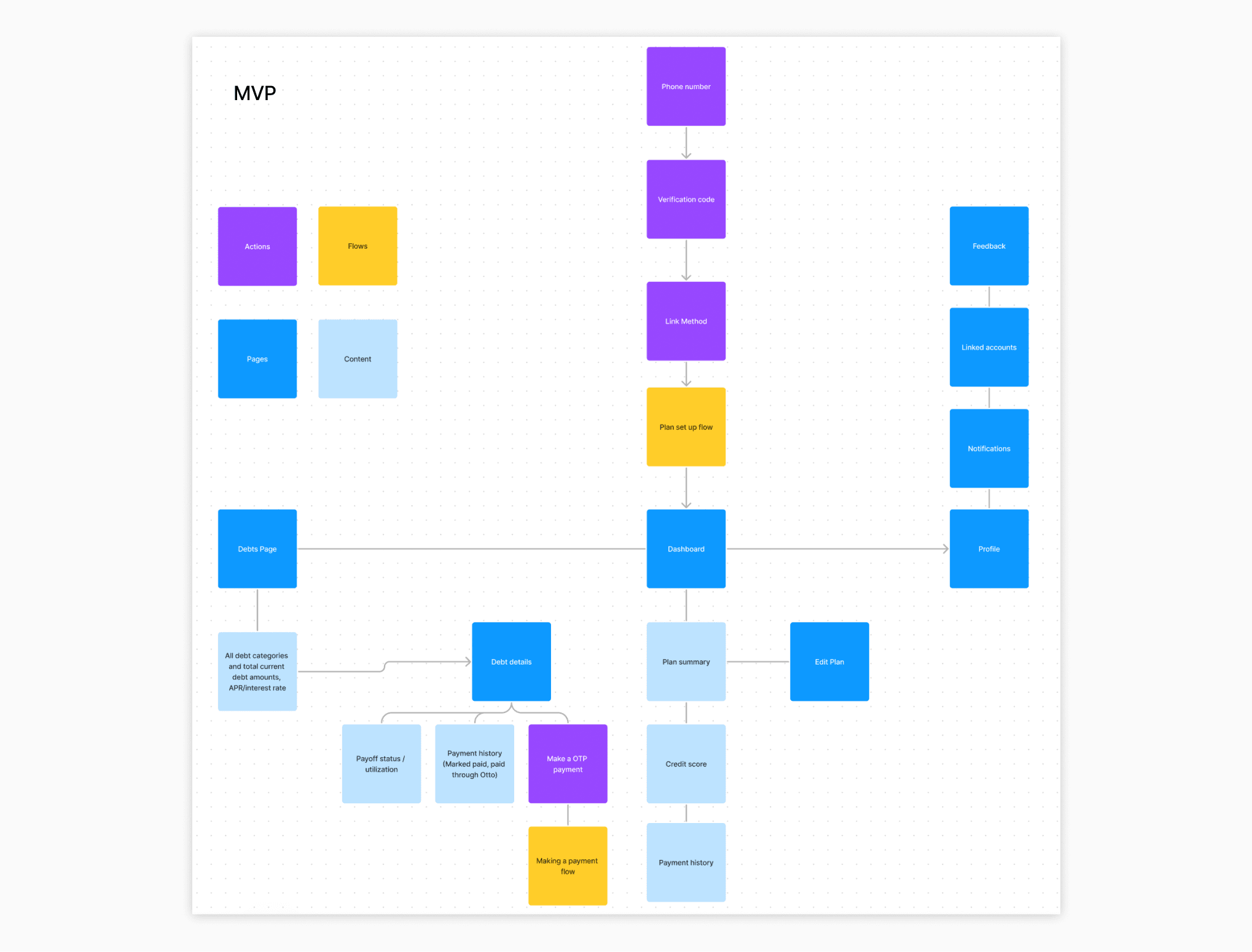

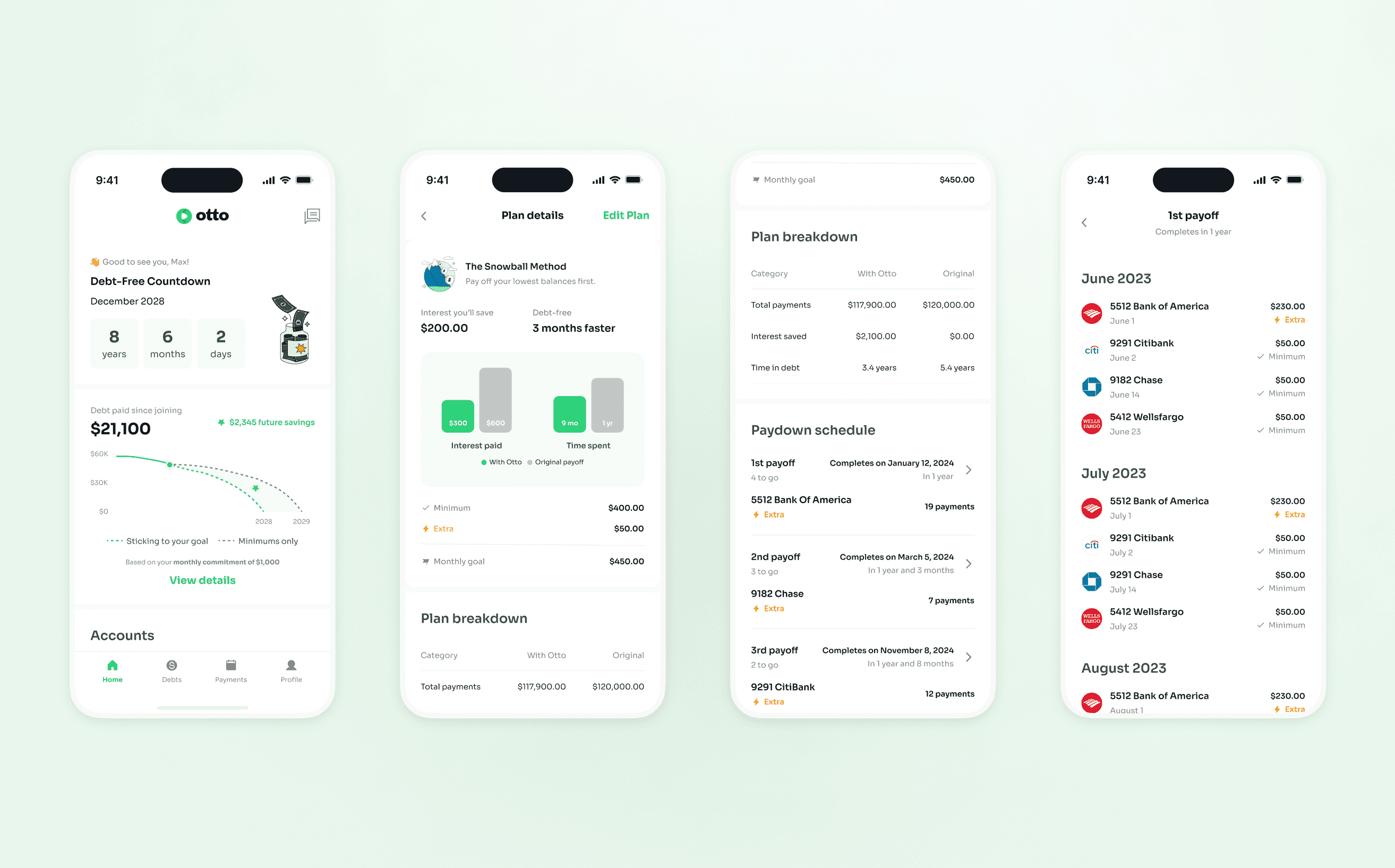

Final solution

Setting users up for success

Final solution

Insights to payoff

Final solution

Recommending payment amounts

Final solution

Birds eye view of their debts